Annuities

Types of Annuities

Fixed or Deferred Annuity:

A fixed Annuity is designed for long term, tax deferred accumulation. Insurance company guarantees both principal and interest. Interest rates are fixed for a certain period of time. Surrender charges may apply for early withdrawal. Some plans allow add-ons. There are no management fees or any upfront costs associated with a fixed annuity. All investment risk with a fixed annuity is absorbed by the insurance company.

Variable Annuities

A variable annuity is also designed for long term, tax deferred accumulation however the investment risk is placed with the investor and thus higher returns are very possible but so is the possibility of principal loss. Money invested goes into a “pool” of Mutual Funds administered by different Fund Managers. Clients are allowed to switch between funds as the market dictates. Variable Annuities will usually have upfront costs, yearly management fees, insurance costs, etc that can dramatically reduce any annual gains realized. Variables also have surrender charges.

Immediate Annuity

An immediate annuity is used to provide a client a guaranteed monthly income for a specific period of time. Time periods are usually for a minimum of 4 years and can be as long as ten years. Since an immediate annuity is a return of both principal and interest, a portion of the monthly check is “tax free”. Once a person deposits money into an immediate annuity, there are no charges allowed, no surrenders possible. At the end of the time period selected the checks stop and the client has no principal left. If the client should die before he reaches the end of his payout period, his beneficiary would receive the monthly payments for the remainder of the selected time period.

Guaranteed Annuity

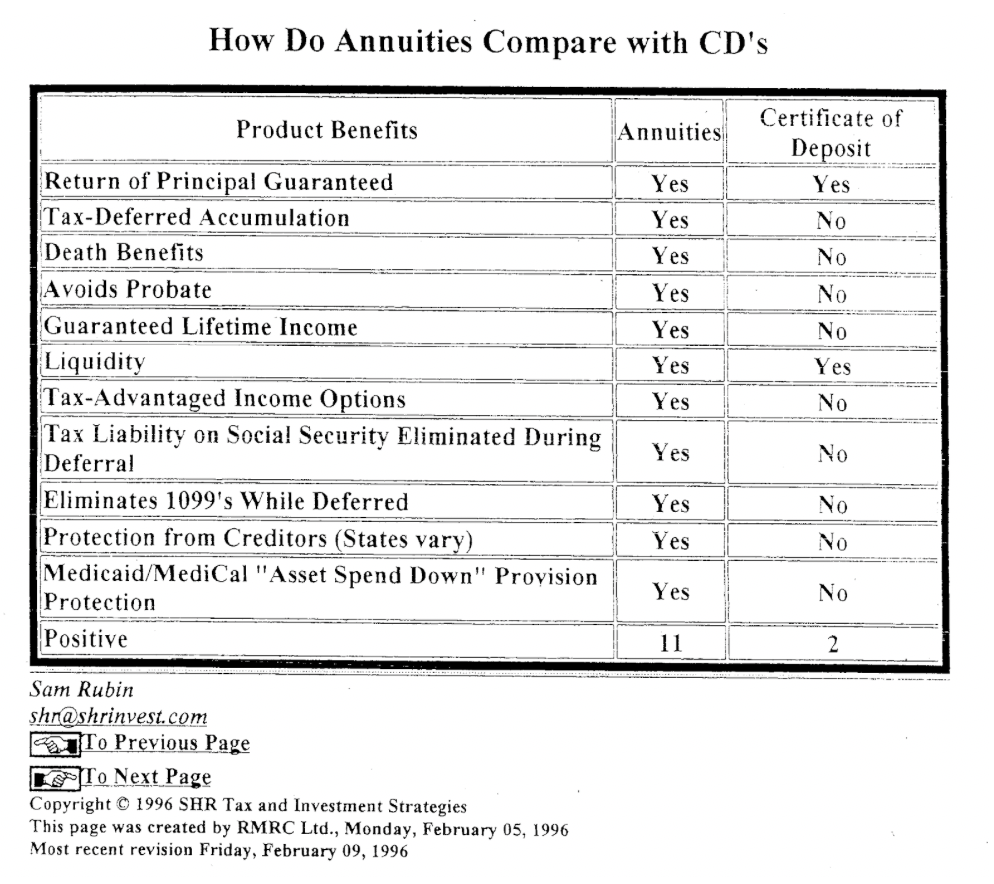

Guaranteed Return Annuities (GRAs) are very similar to traditional bank CDs. The interest rate is guaranteed and the principle is never at risk. One of the many key features of a GRA is that the interest earnings are completely TAX DEFERRED, which allows your funds to grow much faster. Plus, GRA interest rates are usually .5% to 1% higher than typical CD or Money Market accounts. When combined with the power of tax deferral means your money can double its value as much as 40% faster.

A GRA is extremely safe: GRAs are backed by some of the nation’s strongest insurance companies. The rate, the principal and the interest earnings are all GUARANTEED by the strong company you select. For added safety, insurance companies must adhere to very stringent reserve requirements and specific regulations by law. On top of that, insurance companies are ranked by the independent rating service A.M. Best (among others) to give investors an understanding of the relative strength and peace of mind before they ever invest.

A GRA offers faster wealth accumulation with tax deferral: Your money can grow 33% faster when it accumulates Tax Deferred. This means that your principal earns interest, your interest earns interest, and the money you would have normally paid to the IRS each year in taxes, earns interest.

A GRA doubles every 8 years vs. 12 years for an equivalent taxable investment @ 9%. A taxable CD earnings 8.5% annually, only nets 5.7% after the taxes are paid each year or every three years, you will pay the equivalent of one year’s interest earnings to the IRS in a taxable account. Not so with the GRA.

A GRA offers reasonable liquidity: Almost all GRAs allow you to access to your funds while they grow. Most plans will allow an annual withdrawal of 10% of the accumulated account each year. Some plans even allow the access to be cumulative up to 50% of the total account value.

A GRA has no sales charge or load: Since a GRA has no sales charges, management fees, or administrative fees of any kind, every penny you invest goes to work for you at the interest rate guaranteed by the insurance company. You may incur a slight surrender charge for early withdrawals (like bank CDs) so be sure to know what the surrender charges are before you invest.

A GRA is very easy to understand: GRAs are simple, conservative and very easy to understand. Once you learn the subtle differences and dramatic benefits a GRA can offer you over traditional taxable investments, you’ll never want to go back again.

Other advantages a GRA offers: Add-Ons – with some plans, as more funds become available you can reposition them into your existing annuity without new surrender charges.

Interest Rate Bailout – Some plans offer an interest rate bailout where if the interest rate ever drops below a certain specified rate, you can bailout and get all your principle and all you accrued interest without penalties whatsoever.

Medical Bailout – Some plans allow you to bailout if you are confined to a hospital or long term care facility for a certain period of time; usually 30 days.

Unlimited Contributions – You can put in as much as you want and gain all the benefits of Tax Deferral, unlike IRAs or KEOGHs or SEPs, etc.

Something else to know when you purchase a GRA: The purpose of a GRA is for long term wealth accumulation. It is not designed nor intended to replace the liquidity of a money market account. If you withdraw funds prior to the end of the surrender period and before age 59 ½, not only will the insurance company impose a surrender charge for early withdrawal, but the IRS will also impose a 10%penalty for an early withdrawal.

More Facts About Annuities

They grow tax deferred. What that means is that the client doesn’t have to pay taxes on their interest until they actually take money out. Which means that their principle earns interest, their interest earns interest, and their money grows a lot faster; which also means that they do not have to pay any money to Uncle Sam until they take it out. By having a tax-deferred account you money grows at a 40%faster rate than if it was in a taxable account. Taxable accounts include the following: Mutual Funds, CDs, savings accounts, checking accounts, money market accounts, and bonds. Non taxable accounts include the following: some government bonds, and some money market accounts. Tax-deferred accounts are the following: annuities, 401ks, IRAs, 403 Bs, stocks and bonds.

Now you do have to pay taxes on the earnings when you take them out but it is much better than having to pay taxes through out the term.

They avoid probate. When a household dies all their assets must go through probate which is what we call the exit fee. The state of California will probate or “freeze” up an estate and by legally saying that their heirs get what they get they charge thousands of dollars. Because annuities have a designated beneficiary they pass by probate and go directly to their beneficiaries.

They are fixed annuities which mean they have a guarantee of principal.

They have a systematic withdrawal schedule which means that the client can take up to 10% of the cash value without having any penalties. They can have the money directly deposited into their account on a monthly basis.

It is an account for people who are looking for safety in their investment. It provides safety along with the potential for double digit income.